Learn how to make a balance sheet presentation for the company. We often see many analyzes of listed companies where they talk about their balance sheet and their economic strength… They tell us about this and other concepts that sometimes we do not understand and therefore we have to make an act of faith in what they tell us.

The function of this tutorial is to explain what the general balance of a company is and how to make a balance sheet presentation. Thus, when they publish their data in the Relevant Events (HR) of the CNMV, we can deduce their results without having to read the news where they make up their numbers.

Go for it:

How to make a balance sheet presentation?

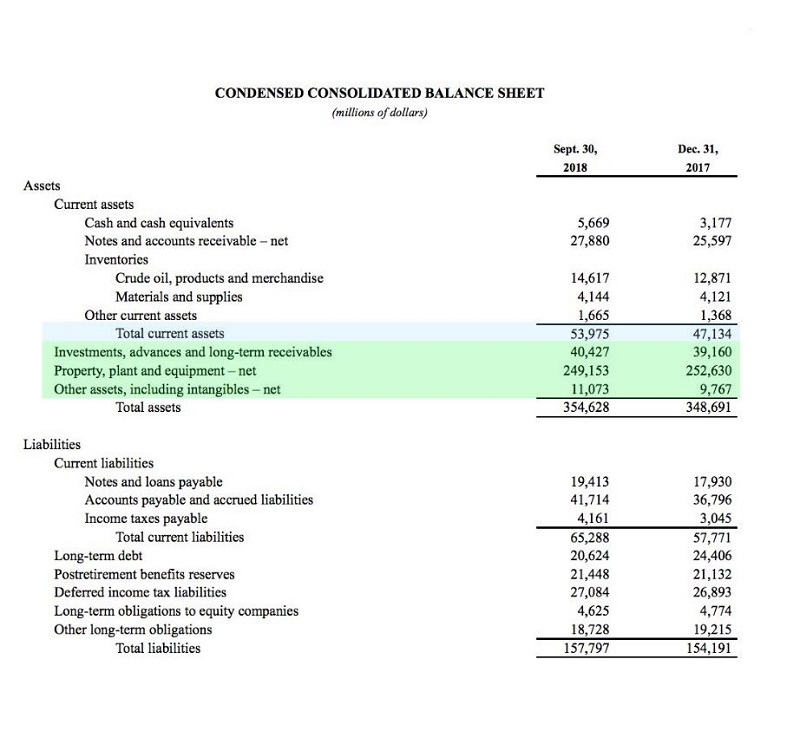

A business balance consists of making a thorough study of all the accounts of a company in order to know its exact status. In this way, we can find out if you can meet the objectives set. In short, It will help us to know if the company enjoys good financial health and its future.

The realization of this balance applies to all types of companies, regardless of their size, and is usually carried out at least four times a year. Every shareholder must (or should) know the balance of the company where he invests. Companies listed on the Ibex must submit their numbers every quarter (or semester) and they are published in the CNMV in the eyes of any investor.

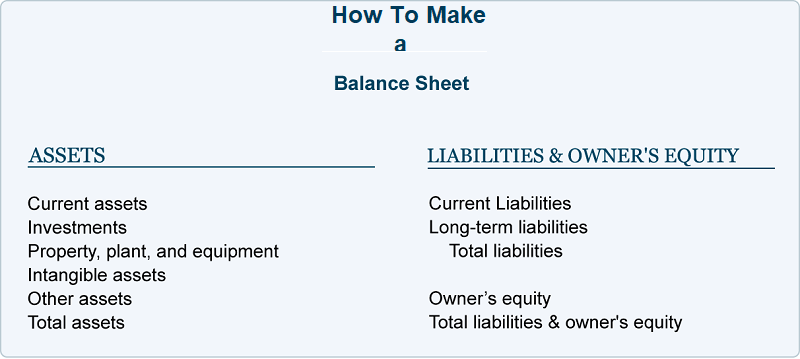

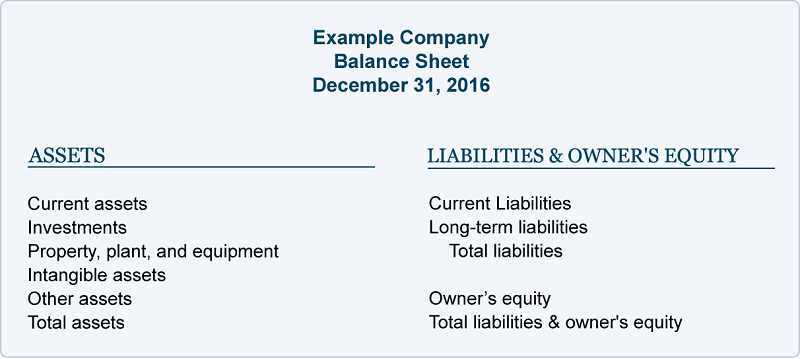

Components of a Balance Sheet

All balance consists of two parts or components:

- ACTIVE: It is defined as active everything that the company owns: rights, assets and other elements and resources that it has.

- LIABILITIES: A liability is defined as everything that the company owes: debts and other obligations with which it finances its assets.

Distribution of the Assets of a Balance Sheet

Within the asset we will distinguish two types:

Noncurrent Asset: Also called Fixed Assets, it is formed by assets with life longer than one year or what is the same, they cannot be realized. This means they cannot be liquidated in a period of less than one year.

Items that make up the Noncurrent Asset:

- Fixed assets: Movable and immovable property, machinery, land, etc.

- Long-term financial investments Term: fixed income securities, capital contributions, and other assets.

- Intangible assets: Patents, industrial property, intellectual property, etc.

Current Asset: Also called Current Assets and are those assets whose degree of realization is a period less than one year.

Items that make up the Current Asset:

- Assets held for sale.

- Short-term Periodization

- Debtors and other accounts receivable.

- Short-term financial investments.

- Stocks

- Treasury

Distribution of the Liabilities of a Balance Sheet

Within the passive we will distinguish two types:

Non-current liability: Also known as long-term debt.

Items that make up the Non-current Liabilities:

- Long term debts.

- Obligations in the long term.

Current Liabilities: Also known as short-term receivables:

Items that make up Current Liabilities:

- Short debts (less than one year)

- Short obligations (less than one year).

Within the Passive balance, is the Net Equity that comes to be the difference between the asset and the liability and it is of vital importance since it will give us the capacity of own financing.

Items that make up Net Worth:

- Own funds

- Capital

- Reservations

- Benefits generated

Analysis of the Financial Balance Sheet

Now we will see which items are the most important in order to analyze the behavior of the company, from the financial point of view.

Generally, a ratio is used to see the capacity to finance its assets and it is the percentage represented by the Own Funds over the total liabilities or assets.

In this case, we will use the previously published data, which correspond to the financial data published in the CNMV by the company Special Ingots for the year 2016.

Own Funds Ratio / Total Liabilities

Own funds represent the part of the capital of the company, which really belongs to the shareholders. The first thing we must calculate is the Net equity divided by the total Liabilities:

Let’s see: 35.749 / 66.409 = 53.83%. With this calculation we see that it is a company with a very important capacity to finance its assets, given that its Net Equity (non-required liability) maintains an adequate proportion of the total balance sheet, which will allow it to finance its assets, without much difficulty. To the extent that the proportion is greater, the data will be more positive.

By way of synthesis, we draw up a table to compare with the previous exercise:

Example Calculation of Own Funds of a Balance

Example of calculation of own funds of a Balance Sheet

Calculation of Debts

Know how to make a balance sheet presentation with calculation of debts. Other items that contain the liability and that we will also measure are the debts, to see the evolution of the same, especially the bank debt. This will tell us if the company is increasing or decreasing its indebtedness. Obviously, the greater the debt, the worse for the company.

For this, we must go to the item of Debts with credit institutions and obligations or other negotiable securities within the section on Liabilities.

As in the previous example, we compared the evolution of the debt with its counterpart in the previous year:

Example of Calculating Debt of a Balance

Example of calculating the Debt of a Balance Sheet

DFN (Net Financial Debt)

Formula for calculating net financial debt (NFD):

DFN = (Non-current financial liabilities + Current financial liabilities) – (Cash and other equivalent liquid assets + Other current financial assets).

Located in the balance in the following headings:

PASSIVE:

1116 Non-current financial liabilities

1123 Current Financial Liabilities

ACTIVE:

1070 Other Current financial assets

1072 Cash and other equivalent liquid assets.

These headings are those consigned by the CNMV, for the consolidated balance sheet of all the companies.

Calculation of Working Capital or Circulating Capital

This calculation allows us to find out the ability of a company to continue with the normal development of its activities in the short term . It is important to verify that the FM is not negative, since this would mean problems when returning the debts in the short term. It is true that in some business activities, it can be considered normal, such as in large supermarkets, where suppliers charge after the customer pays cash.

To calculate the Working Capital Fund or working capital, we will subtract the Current Asset from the Current Asset.

MANEUVER FUND = CURRENT ASSETS – CURRENT LIABILITIES.

In the balance of the example we will obtain the following amount:

Current assets 27,886 – Current liabilities 24,594 = 3,292 working capital or positive working capital of 3,292 million euros.

Other details to keep in mind

To know how to make a balance sheet presentation, we will pay special attention to the quality of your assets: land, facilities and everything that makes up the fixed assets. Likewise, we must monitor the customer account, which must maintain an adequate percentage of its total sales. A very high customer account without increased sales can mean collection problems.

We will not forget for its importance, its Treasury (Financial Investments, Cash and Banks) which allows us to SEE YOUR LIQUIDITY and affects your Net Debt, which is another of the variables that are normally measured.